First-time buyers will only be required to have a deposit of 10 per cent regardless of the value of a property when applying for a mortgage, as a result of a decision by the Central Bank to relax its macroprudential rules. This is a shift from the current requirement, which puts the ceiling at 90 per cent for loans up to €220,000 but at 80 per cent for the balance of loans above that level.

This means that first-time buyers will be able to borrow up to 90 per cent of a value of a home. The 20 per cent minimum deposit requirement (ie maximum loan-to-value ratio of 80 per cent) continues to apply to second and subsequent buyers. The 3.5 times ceiling on the loan-to-income ratio remains unchanged. Requirements for buy-to-let borrowers and the exemptions for negative equity mortgage borrowers from the measures also remain unchanged.

Speaking to reporters at a press conference announcing the changes, Central Bank governor Philip Lane warned the rules “can be tightened if there is emerging evidence of elevated risks in the mortgage market”.

“The measures are designed to ensure lower resilience, but they are also designed to ensure banks lend sensibly and that excess credit does not build up within the Irish financial system,” he said.

“The evidence shows that the probability of default for mistakes brought out under the measures [brought in last year] is lower.”

Mr Lane also said the change to the €220,000 threshold was partly due to the fact that it would otherwise need regular updating as house prices, incomes and other factors evolve.

“While rising incomes typically might support some gain in house prices, the prospect of future expansion in housing supply and tightening global conditions for lenders are significant factors that may place downward pressure on house prices over the medium term,” he said.

Asked whether the Central Bank had bowed to political pressure to relax the rules, Mr Lane said submissions from all quarters were “taken seriously” but insisted the bank “is independent”

It is “not trying to determine house prices” but that if it observes a “perverse” relationship between house prices and credit growth, it can intervene.

The Central Bank says the review affirms that the overall framework is appropriate and the measures are contributing to financial and economic stability, reducing the risk of unsustainable lending and borrowing.

In addition, 5 per cent of the value of new lending to first-time buyers will be allowed above the 90 per cent LTV limit, while 20 per cent of the value of new lending to second and subsequent buyers for primary residences will be allowed above the 80 per cent LTV limit. Previously, the level was 15 per cent across the board. The current two-month valuation period will be extended to four months in recognition of the fact that a portion of house sales can take longer than the average three months to conclude.

All changes will be effective from January 1st, 2017. The mortgage rules were introduced in February 2015.

Mr Lane said the full effect of the measures will only come into play during the next downturn in the property market. The dominant factors behind house price growth, he said, are that the economy and incomes are growing.

The relaxing of the rules “does not take away” from the responsibility of banks to “lend prudently” and for borrowers to borrow prudently.

He added the mortgage review will examine the macro financial situation whereas Wednesday’s review dealt more with the operational framework of the rules..

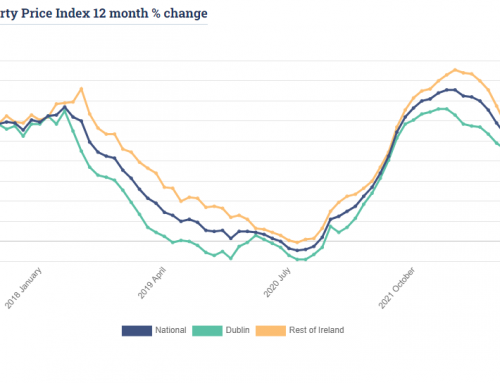

The median house price in Dublin today is €280,000 compared to €220,000 in 2013.

Article by Ciarán Hancock, Joe Brennan – The Irish Times